Table of Content

Table of ContentEvery month, Sarah watches her accounting team drown in paperwork. Invoices pile up. Vendors call asking about late payments. Her team spends hours manually entering data, cross-checking numbers, and chasing down approvals. The irony? Her company processes millions in revenue, but their payment system looks like something from 1995.

She's not alone. Thousands of businesses are hemorrhaging time, money, and sanity because their payment processes haven't caught up with the digital age. The problem isn't just inefficiency, it's the hidden costs that don't show up on any balance sheet. Lost early payment discounts. Damaged vendor relationships. Employee burnout from mind- numbing data entry. Security risks from manual handling of sensitive financial information.

But here's the good news: companies that modernize their payment operations see dramatic improvements. We're talking 75% reduction in processing time, 90% fewer errors, and significant cost savings. The technology exists. The solutions work. The question is simply whether you're ready to leave the paper chase behind.

This guide breaks down exactly how modern businesses are transforming their payment operations, what technologies actually move the needle, and how you can implement changes without disrupting your day-to-day operations. No fluff, no vendor pitches, just practical insights from companies that have made the leap and lived to tell the tale.

The Real Cost of Outdated Payment Systems

Let's talk about what manual payment processing actually costs. Most finance leaders focus on the obvious expenses: staff time, paper, postage. But those are just the tip of the iceberg.

Consider the accounting department at a mid-sized manufacturing company. They process about 500 invoices monthly. Each invoice takes roughly 15 minutes to handle manually, opening mail, data entry, routing for approval, filing. That's 125 hours of labor every month, or more than three full-time employees just pushing paper around.

Now multiply that by your team's average hourly cost. Add in the overtime during the month-end close. Factor in the time spent hunting down lost invoices or fixing data entry mistakes. You're likely looking at six figures annually, and that's before considering indirect costs.

The indirect costs hurt worse. Late payment fees add up quickly when invoices get lost in email chains or sit on someone's desk waiting for approval. Early payment discounts slip through your fingers because you can't process invoices fast enough to capture the 2/10 net 30 terms. Your cash flow forecasting becomes guesswork because you don't have real-time visibility into what's been paid, what's pending, and what's overdue.

Then there's the audit trail problem. When regulators or auditors come knocking, can you quickly produce documentation for every payment? Manual systems make this painful. Files get misfiled. Email approvals disappear into deleted folders. Paper receipts fade or get damaged. You end up paying consultants hefty fees to reconstruct your payment history.

Security vulnerabilities multiply with manual processes too. Paper checks can be intercepted, altered, or forged. Email invoices and payment instructions get compromised in phishing attacks. When payments flow through multiple hands and systems, each touchpoint creates an opportunity for fraud or error.

The human toll matters as well. Your accounting team didn't sign up to be data entry clerks. They have skills and knowledge that could add real value to your business, if they weren't spending 80% of their time on administrative grunt work. High turnover in accounts payable departments often traces back to job dissatisfaction from repetitive, low-value tasks.

The Digital Payment Revolution Nobody's Talking About

Most business owners think of payment modernization as simply switching from checks to ACH transfers or credit cards. That's like thinking the internet is just for sending faster telegrams. The real transformation happening in B2B payments goes much deeper.

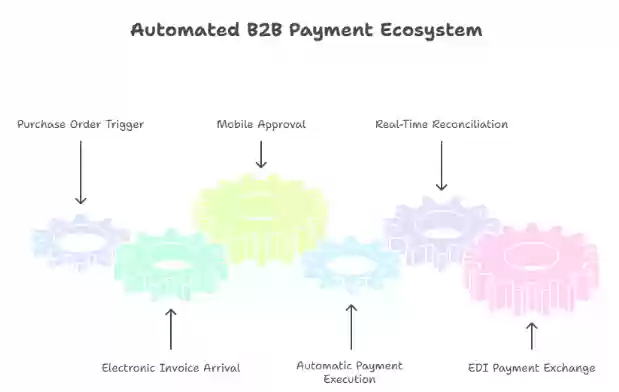

Smart companies are building end-to-end automated payment ecosystems. Purchase orders trigger automatically based on inventory levels. Invoices arrive electronically and flow directly into accounting systems. Approvals happen via mobile apps based on predefined rules and thresholds. Payments execute automatically on optimal dates to maximize cash flow while capturing early payment discounts. Reconciliation happens in real-time without human intervention.

This level of integration requires more than just digitizing existing processes. It demands rethinking how financial data flows through your organization. That's where specialized payment protocols make the difference.

Electronic Data Interchange represents one of the most powerful tools in this arsenal, though it often flies under the radar. If you're wondering exactly what this technology entails, Orderful explains EDI payments meaning in detail, essentially, it's a standardized way for businesses to exchange financial documents and payment information directly between computer systems, eliminating manual data entry and reducing errors dramatically.

The beauty of these automated systems lies in their precision. When your ordering system talks directly to your vendor's invoicing system using standardized protocols, there's no room for typos, transposed numbers, or miscommunication. The invoice amount matches the purchase order. Payment terms are clear from the start. Both parties have the same transaction data in their systems simultaneously.

This level of integration creates something accounting teams rarely experience: confidence in their data. You know your accounts payable balance is accurate because it's calculated from source data, not manually entered numbers. You can trust your cash flow projections because they're based on actual payment schedules, not estimates. Your financial close process shrinks from days to hours because there's nothing to reconcile, the data was synchronized all along.

The competitive advantages extend beyond the accounting department. When you can process payments faster and more reliably, you become a preferred customer. Vendors offer better terms. You can negotiate volume discounts knowing you can track and validate them. Your supply chain becomes more resilient because you have real-time visibility into every financial commitment.

Building Your Payment Modernization Strategy

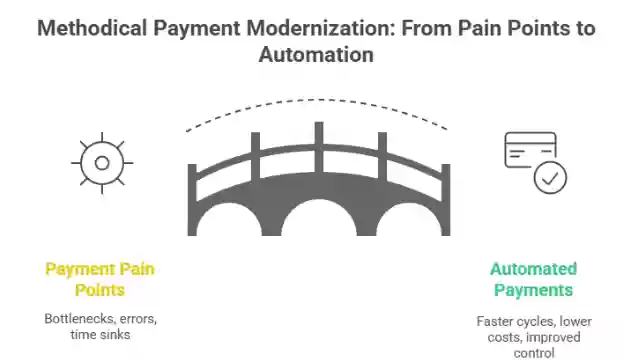

Transforming your payment operations isn't about ripping out everything and starting from scratch. The companies that succeed take a methodical, phased approach that delivers quick wins while building toward comprehensive automation.

Start by mapping your current payment journey. Document every step from the moment a purchase order goes out until payment clears and reconciliation is complete. Identify the bottlenecks, error-prone steps, and time sinks. You'll probably find that 80% of your pain points cluster around a few specific processes.

Most organizations discover their biggest opportunities in invoice receipt and data entry. Switching to electronic invoice delivery solves multiple problems at once. No more lost mail. No data entry errors. Invoices route automatically to the right approver based on predefined rules. The cost per invoice processed drops from dollars to pennies.

Approval workflows deserve special attention. Traditional systems force invoices through rigid approval chains regardless of amount or risk level. Modern platforms use intelligent routing, small routine purchases get approved automatically, while unusual or high-value transactions escalate to appropriate decision-makers. This dramatically speeds up payment cycles without sacrificing control.

Payment execution offers another high-impact target. Most companies still cut checks for a significant percentage of their payables, despite checks costing $4-7 each to process versus under $1 for electronic payments. Transitioning vendors to electronic payments delivers immediate, measurable savings.

The key is sequencing these changes thoughtfully. Pick a pilot group, maybe your top 20 vendors by volume or a single department, and implement comprehensive automation for that subset. Work out the kinks in a controlled environment before rolling out organization-wide. Use the pilot results to build internal support and refine your processes.

Change management matters more than technology selection. Your team needs to understand why you're changing processes and how it benefits them personally. Nobody gets excited about new accounting software, but they do get excited about eliminating tedious work, reducing stress during month-end close, and having time for more interesting projects.

Vendor management is the other critical success factor. Your suppliers need to adapt to your new systems, which means some will need support and incentives. Consider offering early payment in exchange for switching to electronic invoicing. Provide clear documentation and maybe even training sessions for key vendors. The investment pays off in faster adoption and fewer support issues.

Measuring Success and Continuous Improvement

Implementing new payment technology is just the beginning. The real value comes from continuously optimizing your processes and expanding automation into new areas.

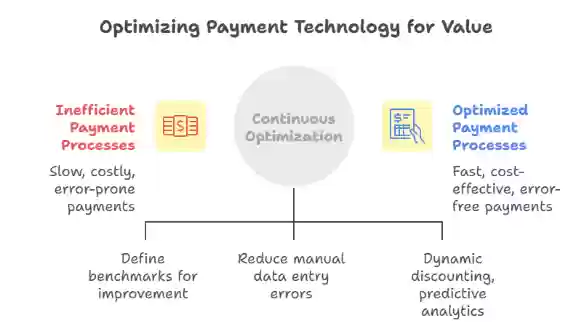

Establish clear metrics before you start. Average invoice processing time. Cost per transaction. Error rates. Early payment discount capture rate. Days payable outstanding. These become your benchmarks for measuring improvement and identifying new opportunities.

Most organizations see dramatic improvements in the first six months. Processing times typically drop 50-75%. Error rates plummet because you've eliminated manual data entry. You capture significantly more early payment discounts because invoices flow through your system faster. These quick wins build momentum and justify further investment.

But don't stop there. As your team gets comfortable with basic automation, look for advanced optimizations. Dynamic discounting programs that offer sliding-scale early payment discounts based on your cash position. Predictive analytics that identify potential payment issues before they occur. Supplier financing options that let you extend payment terms while vendors get paid early.

Integration opportunities expand as more of your business systems become digital. Your payment platform can talk to your inventory system, triggering orders automatically when stock gets low. It can integrate with your procurement system, ensuring purchase orders and invoices always match. It can feed data into your business intelligence platform, giving executives real-time visibility into spending patterns and cash flow.

The most sophisticated organizations treat their payment infrastructure as a competitive weapon. They use the data flowing through their systems to negotiate better terms, identify cost-saving opportunities, and build stronger supplier relationships. They can offer suppliers multiple payment options, traditional terms, early payment at a discount, or dynamic discounting, and let each vendor choose what works best for them.

This flexibility transforms the vendor relationship from transactional to strategic. Your suppliers know they can count on accurate, timely payments. They see you as a professional, well-run organization. That goodwill translates into better service, priority during shortages, and willingness to work with you on custom solutions.

Taking the First Step Toward Payment Transformation

The gap between outdated payment processes and modern automated systems isn't just about technology, it's about business performance. Companies stuck in manual processes spend more, move slower, and face greater risks than their digitally-enabled competitors.

But transformation doesn't require a massive upfront investment or complete system overhaul. The path forward starts with small, manageable steps that deliver immediate value while building toward comprehensive automation.

Begin with assessment. Spend a week tracking how your current payment process actually works. Time each step. Count the handoffs. Document the pain points. You'll likely find that reality differs significantly from what you assumed. This data becomes your baseline and helps you prioritize improvements.

Next, identify your lowest-hanging fruit. For most organizations, that's electronic invoicing and basic approval automation. These changes don't require expensive software or extensive integration work, but they eliminate significant manual effort and deliver measurable cost savings within months.

As you build momentum, expand into more sophisticated automation. Electronic payment execution. Automated reconciliation. Intelligent routing and exception handling. Each layer adds value and prepares your organization for the next step.

Remember that payment modernization isn't just an IT project, it's a business transformation that touches procurement, accounting, treasury, and vendor management. Success requires executive sponsorship, clear communication, and realistic expectations about timeline and effort.

The businesses that thrive in the coming years will be those that treat financial operations as a source of competitive advantage rather than a necessary evil. They'll leverage technology to eliminate waste, improve visibility, and build stronger relationships with suppliers and partners.

Your payment process represents thousands of interactions annually with the vendors, service providers, and partners that make your business possible. Each interaction is either strengthening those relationships or damaging them. Each transaction is either running efficiently or wasting resources. The choice is yours.

The technology exists. The business case is proven. The only question is whether you're ready to stop accepting the status quo and start building a payment operation that matches your ambitions for your business.